Looking back at 2025, as the transitional implementation year for the "reverse invoicing" policy, the National Development and Reform Commission's "Document No. 770" explicitly required the termination of local governments' non-compliant investment promotion cooperation. Under the policy guidance of building a unified national market, the copper scrap industry has been gradually moving toward a standardized and compliant development track.

In 2026, the "reverse invoicing" policy will enter the full implementation stage. Compared with the transitional period in 2025, oversight by the tax authorities will become more in-depth and refined: first, strengthening the review of whether invoicing enterprises are real operating entities and eliminating shell company operations; second, requiring the invoicing party to have actual business premises, with addresses used solely for invoicing and fund transfers to be deemed false invoicing; third, strictly enforcing the alignment of the "three flows"—capital flow, invoice flow, and goods flow—to ensure a complete closed loop for business transactions.

"Migratory bird" enterprises that previously relied on illegal local government "awards and subsidies" will find it difficult to continue from 2026 onward. The "invoicing economy" model has already been halted, and at the local level, any form of illegal fiscal rebates or disguised reductions and exemptions is prohibited. Once discovered, violators will face severe penalties from relevant national authorities.

"Reverse invoicing" not only addresses the long-standing problem of missing input invoices for copper scrap, but also serves as an important basis for verifying the authenticity of enterprise business operations. According to policy guidance, after resource recycling enterprises issue invoices to natural-person sellers, they may credit 1% of the output VAT payable as stipulated; meanwhile, recycling enterprises are required to prepay individual income tax for the natural-person sellers at 0.5% of sales revenue, thereby making the tax burden of transactions clearer and more transparent.

The policy further requires enterprises to establish standardized purchase ledgers and to record each transaction process through photos, videos, and other means. Once false invoicing is discovered, enterprises may not only be required to pay back taxes and fines, but may also bear criminal liability.

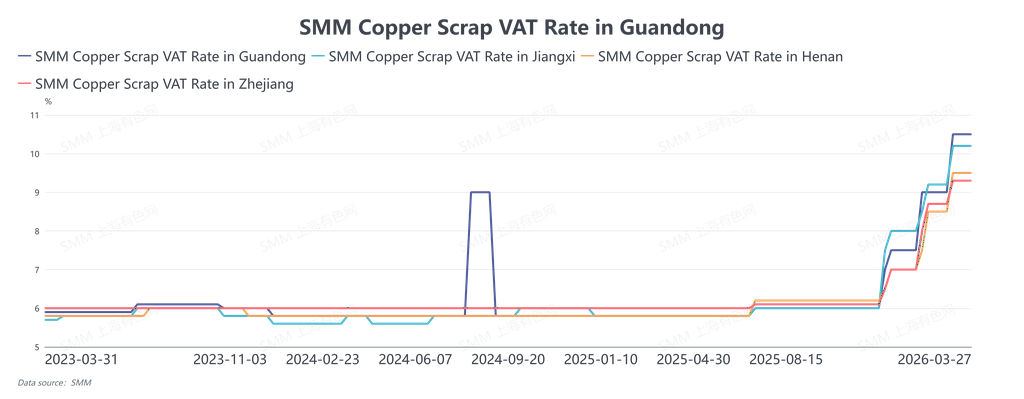

According to the SMM survey, more and more enterprises have begun implementing the requirements of "reverse invoicing." However, due to the limited invoicing quota that natural-person sellers can provide, and the fact that the total annual "reverse invoicing" quota for a single enterprise does not exceed 5 million yuan, many enterprises have had to turn to imported or domestic VAT-inclusive copper scrap as a supplement. As demand for VAT-inclusive supply continues to grow, its price cost has kept rising, and on some trading days, VAT-inclusive bare bright copper prices have even inverted against copper cathode prices. In 2026, the market landscape will undergo profound changes, with enterprise competition shifting from “competing on subsidies and incentives” to “competing on energy efficiency”:

Against the backdrop of a unified national market, the differences in raw material and finished product quotations previously caused by differentiated local subsidies and incentives will gradually disappear, and the flow of copper scrap will return to the fundamentals of supply and demand and the logic of transportation costs.

Following the standardization of compliant operations, enterprises’ efficiency in the use of capital, access to bank credit support, and supply chain financing capabilities will become key competitive strengths. Amid price fluctuations, whether enterprises can seize spot opportunities by leveraging cost advantages in capital will directly affect their profitability.

Non-compliant shell resource recycling companies and “migratory bird” producers will exit the market in a concentrated manner. Only legitimate producers that meet the filing and approval requirements of the Ministry of Industry and Information Technology will be able to participate in fair competition in the future market.

In short, in 2026, the copper scrap market is moving toward greater standardization and transparency. As national policies continue to improve, the “red lines” for enterprise operations are becoming increasingly clear, and compliance has become a prerequisite for survival and development. Only by understanding policies and making good use of the rules can enterprises make steady and sustained progress in this industrial transformation.

![Copper Inventories in Major Regions of China Continued Destocking During the Week [SMM Weekly Data]](https://imgqn.smm.cn/usercenter/gCNEi20251217171715.jpeg)